Brexit’s Unwanted Birthday Present

Not even ‘Project Fear’ saw this one coming

Chris Johns

Rishi, the worst is yet to come, you have Brexit to thank for it, and be careful when you welcome wage rises.

Brexit is the gift that keeps on giving. Tying up Westminster in years of endless rows, negotiations (external and internal) and rafts of new legislation (or not, in the case of abolishing and replacing EU laws). Multiple Prime Ministers, Chancellors of the Exchequer, Home Secretaries, Foreign Secretaries. When even Nigel Farage says “Brexit has failed” you have to wonder at those who still express true belief. I could make a long list of all the impeccable research that calculates the economic damage but I will resist that temptation. My own view is the collapse in UK governance and the ongoing ruptures to British civil society are actually worse than dry calculations of export losses and GDP reductions. Just don’t ever mention Brexit in polite company

I’ve written extensively on this platform about all of the suspects that have driven the UK economy’s dismal 15 years (here, here and here, amongst many pieces). In this post I will try and do a couple of things. First, there is the economic problem - inflation - that is afflicting Britain in a bigger way than most other developed economies. I want to to this in as straightforward a way as possible, without the usual rehearsal of dry economic statistics that seek to explain that poor performance. That’s to try and achieve my second goal: to describe a big problem that is currently evident and then to suggest that an even bigger issue that is coming the UK’s way.

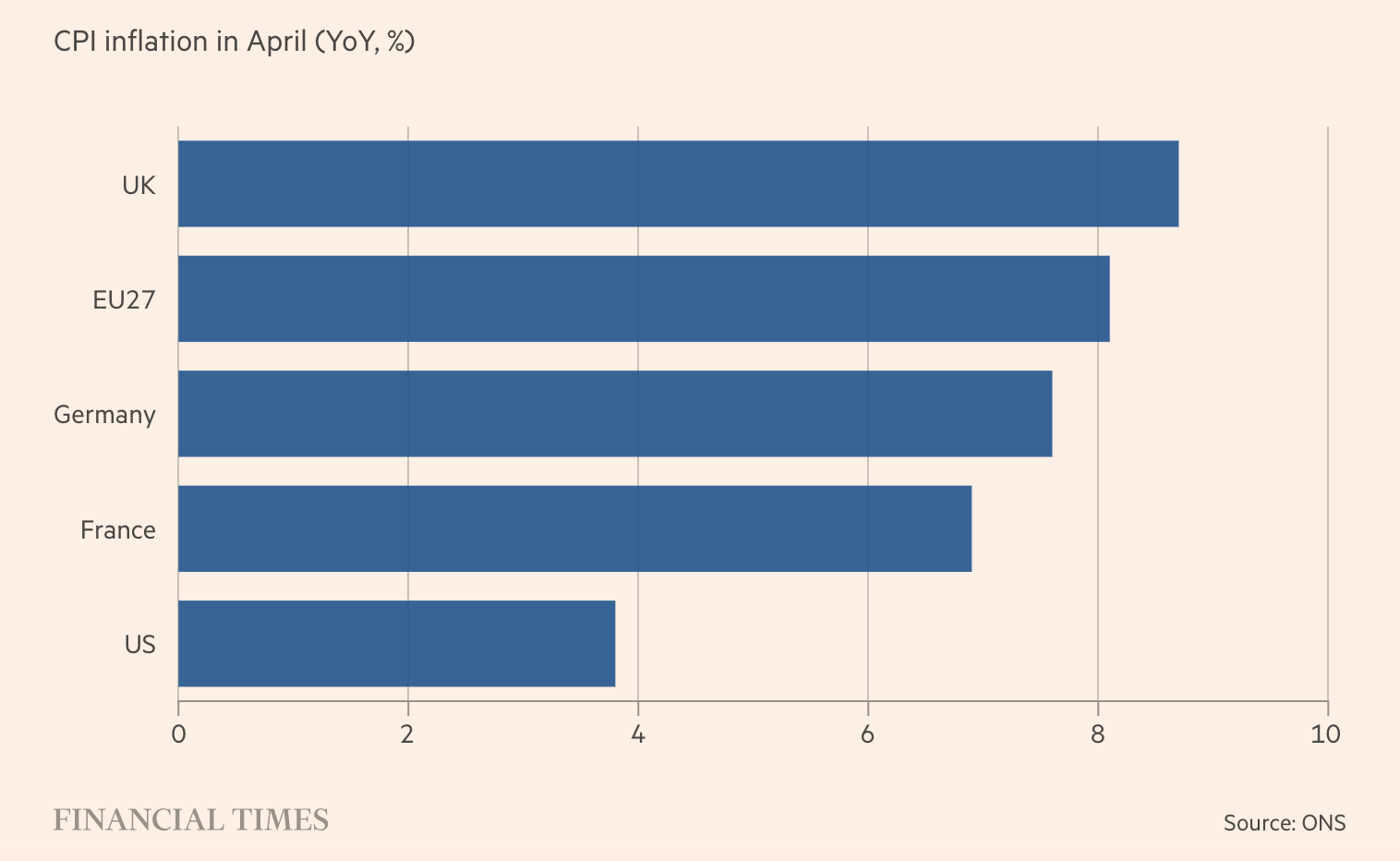

The problem as it stands: Inflation rates compared

The chart explains why investors think that the UK is still quite a way from the peak in interest rates, why the EU is a bit nearer its own peak - but us still not there yet - and why the US Federal Reserve is probably close to at least a pause in raising rates, if not actually at the peak (an interest rate decision is imminent at the time of writing).

There is a list of usual suspects about why the UK is in such a poor relative position. It is alleged, for example, that the energy crisis hit the UK more than other countries because of poorly designed and late energy subsidies for consumers. Also, UK households are said to live in particularly poorly insulated homes, increasing their vulnerability to the energy shock. There is probably something in all of this, but it is hard to establish, with precision, just how much.

Digging into these headline numbers reveals the following:

It’s those measures of services and core inflation the will disturb the Bank of England. They hint - quite strongly - that inflation is becoming ‘embedded’ in the economy. In particular, the extraordinarily tight labour market is giving rise to unwelcome, from a Central Bank perspective, wage rises.

Curiously, Rishi Sunak proudly boasted at Prime Minister’s Questions about ‘strong wage rises under this Conservative government’ which is empirically true but probably disastrous for him. The Bank of England will be appalled by those wage rises and what they might mean for future inflation. Sunak has promised to halve inflation by the end of 2023, something which becomes more difficult (although not impossible) with accelerating wages. The Bank of England Governor this week notably gave no assurances when asked if Sunak’s inflation target would be met.

Here’s the thing troubling the BoE and freaking out the government bond market: wage inflation.

The bottom two lines are two measure of wages expressed in real terms. Note that they are negative - real wages are falling. Sunak celebrated the top two lines: rising nominal earnings.

Why is the UK labour market behaving in this way? The economy has been flatlining for years, yet unemployment remains at historic lows, employers complain they can’t find enough workers and are having to raise wages to attract and retain staff.

Of course, many developed countries have similar problems, but why are they so much worse in the UK? One suspect stands out: Brexit. I know, it’s the taboo subject, beyond boring, a social faux pas to even mention the word. But Brexit has made the most unexpected contribution to the UK’s wage inflation problem, one that even ‘Project Fear’ didn’t foresee.

‘Low wage’ immigration has all but stopped and many exporters to the UK have decided the game of supplying UK consumers is no longer worth the candle. The shortage of workers experienced by the UK is worse than elsewhere and one or two trade barriers have been erected (the B word again). That means foreign imports either cost more or are just unobtainable. Just wait until those trade barriers are properly erected.

This is how the all important government bond market has been reacting to the unfolding inflation - wage inflation - story:

The last time the UK bond market behaved like this was when it blew a gasket after the disastrous Truss-Kwarteng mini-budget of last Autumn. That led directly to Truss’s demise and a near-death experience for the UK pension fund industry - which had to be rescued by the Bank of England. We can only hope that pension fund managers are better prepared now.

Those higher government borrowing costs have all sorts of implications. One obvious problem is increased debt servicing charges, reducing the scope for promised tax cuts ahead of the next general election. The other threat, much more ominous, is to mortgage costs. Lenders have been rapidly pulling fixed rate mortgage products as their costs have risen with those government bond yields and a rising implied path of future Bank of England policy rates.

This chart is taken from the daily missive of Bloomberg’s John Authers (always worth a read for anyone with an interest in financial markets).

This illustrates how what investors think is going to happen to short term interest rates. These are bets - they could be right or wrong. But expectations for interest rates through to the end of the year have been shooting upwards. If these expectations are right, this is terrible news for anyone thinking of taking our a mortgage, anyone on a variable rate mortgage and, crucially, anyone facing an end to their current fixed rate deal.

One of the new features of the UK mortgage market is the rise of the fixe rate deal. Everyone used to be on a variable rate but no longer. More and more householders have fixed their mortgage, usually for two or five years.

The implications of all those fixed rate mortgages have been explored by me on a previous podcast. The Resolution Foundation has done a splendid job detailing why the fixed rate thing is so important:

“Around half of households with a mortgage have yet to see their rate change since the Bank of England started raising rates”

That’s because they fixed their mortgage a while ago. These household are in for a shock when they have to remortgage/renegotiate their deal.

The chart is taken from a report written a month ago when the Bank of England was thought to be much nearer the peak in interest rates than it is now. So all of the mortgage problems forecast by the RF are now likely to be worse:

While around three-quarters of the aggregate increase in repayments will fall on households in the top two income quintiles, households with bigger mortgages relative to their income will be disproportionately affected by higher rates. That means poorer and younger households will be hit the hardest on average. Looking ahead to Q4 2026, when the adjustment to higher rates will be mostly complete, repayments are to set to have increased by more than 4 per cent of income for mortgagors in the second income quintile, compared to just 2 per cent for mortgagors in the top income quintile. And repayments are projected to increase by 3.4 per cent of income for 18-34-year-old mortgagors, nearly double the 1.8 per cent figure for mortgagors aged 55 and above. So while rate rises look likely to be coming to a halt shortly, much of the pain they bring for some UK households is very much still to come.

All of those numbers cited by the RF can be summed up as ‘lots of mortgage agony ahead, particularly for poorer households’. The housing market could be headed for very big trouble. If the worst comes to pass, a housing crisis could take the UK economy into recession, something much forecast but so far avoided.

Rishi, the worst is yet to come, you have Brexit to thank for it and be careful when you welcome wage rises.

I had an email from a UK book supplier this morning telling me that they've opened a warehouse in The Netherlands, and that I should confidently place my orders with them as they will be duty free and will get to me faster than from the UK (I had stopped using them for these very reasons). Another brexit benefit, but for an unintended recipient.

Meanwhile, the brexit slow puncture continues... 🤯

Well, Shane, that's a fine example of the free market working...for you and The Dutch.., that is...