Buoyant stockmarkets and the third wave: will there be a reckoning?

Short memories or long knives?

Chris Johns

Will Europe’s Third Wave Cause a Political and/or Economic Crisis?

It would be easy to conclude that Europe has failed the Covid test. Many countries are experiencing a third (at least) wave of the virus. There is an ongoing and unseemly row - blame shifting mostly - about who did what and when with respect to vaccine procurement and delivery.

Failure and incompetence are charges levelled at the European Commission, particularly its hapless president, and at national governments. When you are criticised by Jean-Claude Junker, a much-mocked former Commission president, you know you are in trouble. I can’t resist quoting some headlines from the EU-phobic British press (with full acknowledgment that most of these organisations are often demented when it comes to their coverage of things EU.)

Even the pro-European Guardian is on the same page:

Normal service from The Sun:

All of these headlines were generated by the attempts of Ursula von der Leyen to deflect responsibility for the agonisingly slow roll-out of the vaccine. Claims that it is all Astra Zeneca’s fault are repeated ad nauseam. I’ve written about this elsewhere. My take is that Europe has at best been naive and, more probably, both incompetent and unlucky. @JimPowerEcon and I have discussed some of the potential political fallout here. Since that podcast, the Astra row has rumbled on and the health situation deteriorated.

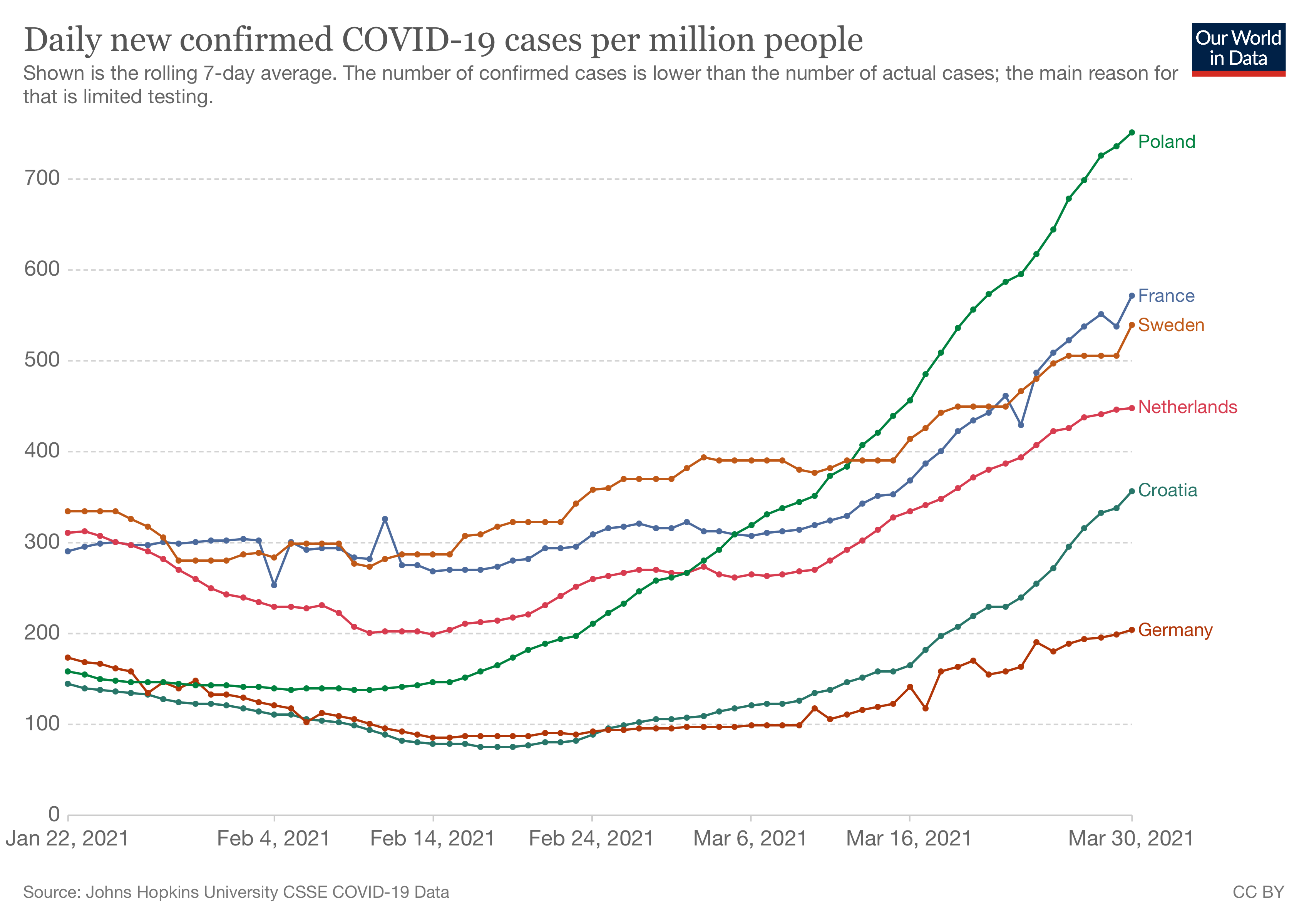

Europe’s third wave is becoming more serious by the day (see Chart 1 below). Political problems are, as a direct result, mounting in various European capitals. This is a headline from the FT, (article here) not known for any EU-bashing tendencies:

The angst is easy to explain. Pictures paint a thousand words:

Chart 1

Germany, as the FT article nicely explains, prides itself on ‘state capacity’, which amounts to a belief, a self-image, that focuses on the ability of government to be organised, competent and able to deliver. And Germany is by no means the worst when it comes to current virus numbers, as graphically described above. Of course, Chart 1 needs its twin, below. This will be familiar enough, although the gaps still have the capacity to surprise. Those gaps between the EU and other countries do tell most of the story.

It cannot be stressed enough: those vaccine gaps will be temporary. Europe will catch up with the US, the UK and Israel. At some point this year, possibly sooner rather than later, rich nations will begin to donate their surplus vaccines (they should, at least).

The question naturally arises: will the pain, angst - and illness- caused by the today’s temporary gaps have a longer term fallout? We can only hazard a guess.

One clue, suggesting that memories will fade, is to be found in the UK. The country with, at the time of writing, the highest death toll in the world is, nevertheless, rewarding the incumbent, responsible, government with a massive ‘vaccine bounce’ in the opinion polls. This suggests that memories, British ones at least, are short.

One thing that the last year has taught us is that things can change very rapidly. The pictures drawn here might look very different, in any one of a multitude of possible ways, in a matter of weeks. But, if the UK and Israel are anything to go by, and their relative success continues, Europe will be be in a much better place in a matter of a couple of months or so. But will politicians be punished for their perceived relative failure?

Chart 2

While there may well be political fallout, the economic consequences of all this are, right now, deemed by investors to be benign. Chart 3 looks at the performance of German stocks over the last 2 years. They are doing very well, suggesting that some people at least aren’t too worried by impending political and/or economic problems.

Chart 3: Germany’s Stockmarket (2 Years to End-March 20201): Unconcerned.

European stock markets may be going up because of the ‘global reflation trade’. Many investors think the great US policy experiment is going to lift all boats. This, of course, is the Biden stimulus: he’s done a lot and is promising even more. But if Europe really was heading into political crisis, at least in the short term, I doubt whether its markets would be quite so sanguine.

It’s that longer term perspective and question about memory that bothers me. Markets can be myopic - short term - and often put future politics in ‘too difficult to think about’ box.

EU memory might be as quick to fade as that of the UK. There may be a seamless transition of power in Germany this summer. The hard right may not do well in next year’s Presidential election inFrance. Sinn Fein may not benefit from the hopeless current Irish coalition government. Maybe.

All of this needs careful watching in the months ahead.