The bond market did it. In any financial whodunnit, it’s always the bond market. UK bond markets were responsible for Liz Truss emulating a lettuce and US bonds (Treasuries) forced Trump to blink.

The initial reaction of stock markets has dominated the headlines but it was the prior behaviour of US bonds that mattered. A proper financial crisis was (or maybe still is) brewing involving loss of confidence in both bonds and the dollar.

Much speculation about a ‘Mar-a-Lago’ accord has been bubbling behind the scenes, echoing decades-old attempts by the US and its allies to manipulate what was seen as a false valuation for the US currency. At least they were allies back then. The really sinister element of the new, rumoured, attempt to mess with dollar included suggestions that Trump will use the trade weapon of mass destruction to force holders of US debt to accept a ‘haircut’. That’s a default in ordinary language. Something that would be truly catastrophic.

The dollar is the world’s reserve currency. A plain vanilla debt default is bad enough - just ask the Greeks or the Argentinians. But a US default would end the reserve status of the dollar. The world does not have a ready made replacement. The resulting financial crisis would make the last one look like a picnic.

My guess is that someone explained this to Trump. It was unlikely to be his coterie of billionaire advisers and cabinet members. The ones who are so disatisfied with modern life they want to blow everything up. Someone, or several people, probably CEOs of large Wall Street institutions, will have been making discreet phone calls.

So we have a 90-day reprieve - unless you are Chinese. What happens next is utterly unknowable. Even Trump has no idea. But he is clearly enjoying the chaos. He is like a toddler running around the control room of a nuclear power plant, unable to resist the buttons and levers marked ‘for emergency only’.

For the sake of m’learned friends, there is no suggestion that Trump or his buddies are engaged in stock market manipulation. There is no way he could have personally profited from the gyrations in the US equity market. But Trump is a terrific financial adviser. As John Authers of Bloomberg points out:

I’ll just leave that there.

If Trump leaves tariffs at 10% they won’t, by themselves, cause a global recession. As Paul Krugman endlessly points out, the Smoot-Hawley tariffs of the 1930s did not cause the great depression. They didn’t help but it was earlier serial policy errors that prompted a global slump.

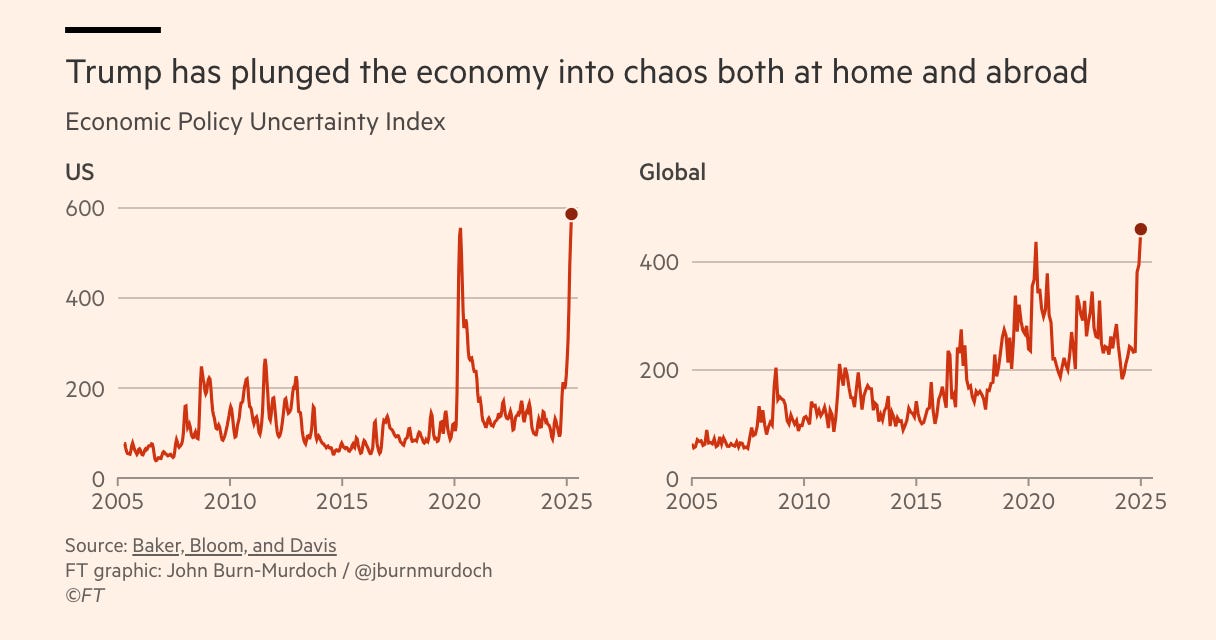

Economists talk about uncertainty all the time. Perhaps to the point of cliché. But uncertainty matters. It is always with us and when it spikes there is always trouble. What we don’t know, in advance, is where the trouble will emerge. But the most stressed parts of the financial system, particularly the bits hidden in dark corners, are usually exposed during times like these.

The policy flip-flops, the policy uncertainty, is an economy-killer. Consumers and businesses will postpone spending and capital investment decisions until uncertainty returns to more ‘normal’ levels. That’s a slowdown in growth. And the more policy chaos lasts, the likelier it is that a slowdown becomes a recession.

Maybe things will settle down. Maybe Trump will stay on the golf course. But buying the stock market today, buying the idea that we are back to normal, means you have to make that bet. I wouldn’t.

Alan Beattie, the FT’s brilliant trade specialist, reminds us almost daily that when it comes to Trump’s tariffs, nobody knows anything.

The comparison between Donald Trump and Liz Truss is now commonplace. To repeat, the common driving factor was the bond market. Martin Sandbu, another must-read FT columnist, reminds us (£) that it is the manner of the policy announcements that matters as much as their content. Sandbu also stresses the important fact that all those associated uncertainty concerns can be measured:

We are dealing with psychology here of course, which is why economists talk about uncertainty with their arms waving madly in the air. It’s mostly about our confidence in the economic future. Things like US consumer confidence levels are falling at rates not seen since the pandemic.

Unlike Truss, Trump is going nowhere. So there is no normal.

Follow us on BlueSky:

@chrisbjohns.bsky.social

@jimpowerecon1962.bsky.social

Take a listen to our podcasts:

The bond markets puts manners on Trump. That’s why they are so efficient , their decision s are based on logic and business and forced Trump to reverse. Something politicians could never do.