EXCHEQUER FINANCES STRONG, BUT COST OF BORROWING RISING

Economic indicators in Ireland are still strong, but careful control of the public finances is essential as long-term bond yields rise

FIRST QUARTER EXCHEQUER RETURNS SHOW IMPRESSIVE TAX REVENUE BUOYANCY

With considerable pressure now coming on government expenditure from factors such as cost of living alleviation measures and the inflow of Ukrainian refugees, it is just as well that tax revenue buoyancy remains the defining feature of the public finances at the moment.

The Exchequer returns for the first quarter show that an Exchequer surplus of €0.2 billion was delivered, which compares to a deficit of €4.2 billion in the first quarter of 2021.

While year-on-year comparisons have to be treated with caution due the fact that the economy was subject to very severe restrictions in the first quarter of 2021, the underlying momentum in tax revenues is very strong.

The key development on the tax revenue front in the first quarter include:

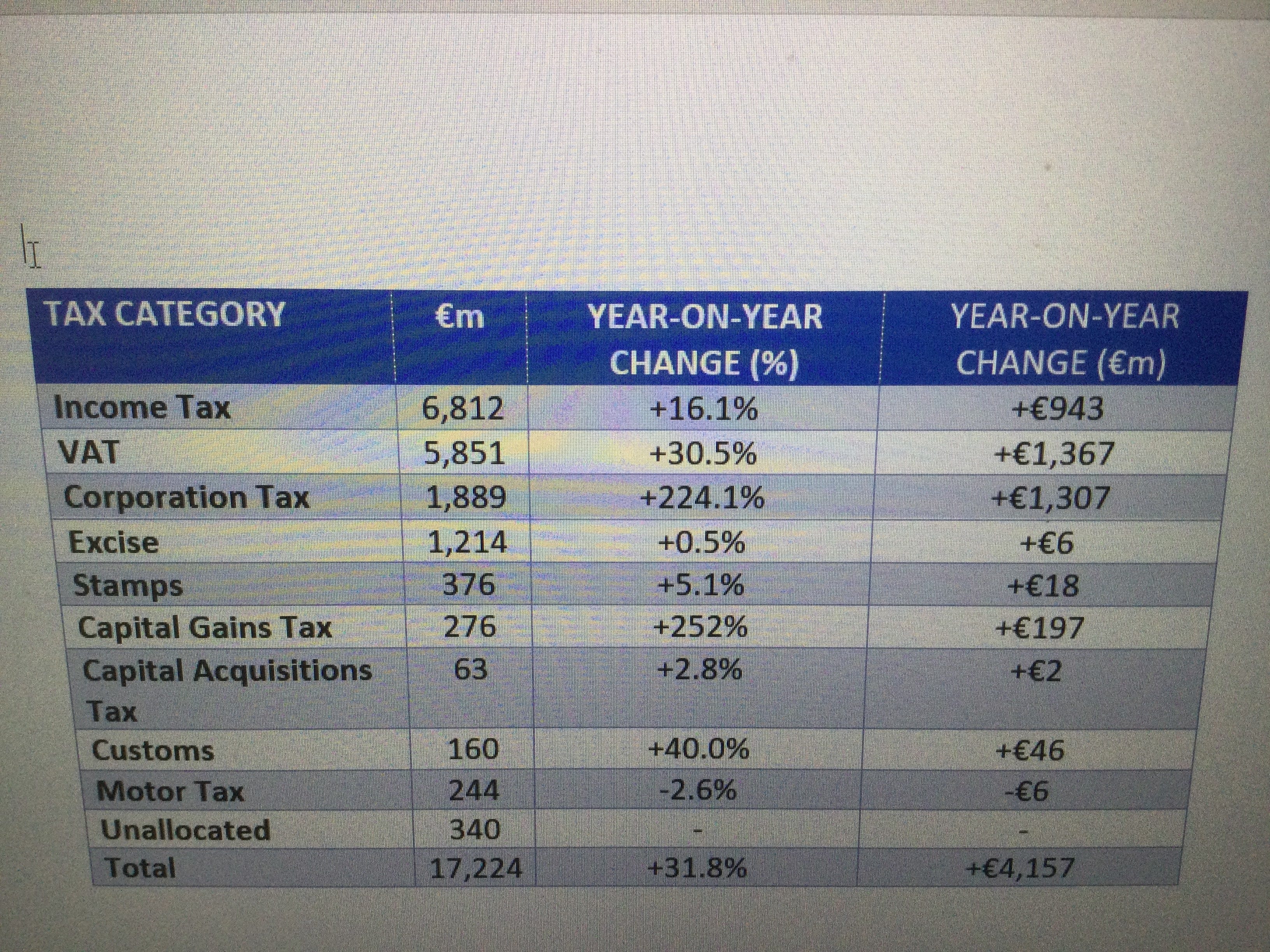

· Overall tax revenues totalled €17.2 billion which is 31.8 per cent or €4.2 billion higher than the equivalent period in 2021. The first quarter of 2021 was distorted by severe Covid restrictions, which exaggerates the annual growth rate. However, when compared to the first quarter of 2020, tax revenues in Q1 2022 were 33.2 per cent higher; and 34.6 per cent higher than non-Covid affected Q1 2019.

· Income tax, corporation tax and VAT accounted for 84.5 per cent of overall tax revenues.

· Corporation tax receipts in the first quarter totalled €1.9 billion, or 224.1 per cent higher than last year. While there are some timing issues here, it also reflects the strong profitability of some of the multi-nationals operating here. Incidentally, the OECD corporation tax reform plan is now under significant pressure

· Income tax came in at €6.8 billion, which is 16.1 per cent or €943 million ahead of 2021. As mentioned, many times before (but it is worth repeating), the strength of income tax receipts reflects the very progressive nature of the Irish income tax system, and the high quality of employment being created in the economy. It is indicative of a very buoyant labour market, where retention, recruitment and increased labour costs are now significant challenges for many employers.

· VAT came in at €5.9 billion, which is 30.5 per cent or €1.4 billion ahead of 2021, when a lower VAT rate applied on a temporary basis.

· Capital Gains Tax receipts are very strong at €276 million, which is 252 per cent ahead of last year, and 53.3 per cent ahead of 2020, and 57.7 per cent ahead of 2019. This may reflect sales of properties and other investments in a strong market, where uncertainties may now be starting to emerge for a variety of reasons.

The overall complexion of the public finances suggests that tax revenue buoyancy will continue to be a feature of the economy in 2022, which is just as well. There is an attitude pervading certain elements of the Irish political system that there are no constraints on the amount of money that Government can spend to alleviate every conceivable problem.

This is a dangerous assertion, because despite what many now argue, debt actually does matter. How much it matters is demonstrated by the recent trend in government borrowing costs. Ireland’s 10-year bond yield currently stands at 1.27 per cent. This is up from 0.25 per cent at the beginning of the year, and zero per cent a year ago, and is the highest level of borrowing costs in six years. While increased bond yields do not affect current borrowing, but over time as fresh borrowing is undertaken and as debt is rolled over and re-financed, the debt servicing burden will rise. This should highlight the risks of continuing to run excessive deficits and the necessity to control spending insofar as is feasible in current economic and political circumstances.

Measures to help those affected by the cost-of-living increases must be targeted and effective. A universal approach is not affordable and will just serve to increase our debt-vulnerability in the longer-term.

LABOUR MARKET UPDATE

Despite the uncertainties surrounding the Ukraine wear and the sharp increase in business and consumer costs, the labour market remains strong. Unemployment at the end of March stood at 146,400, which is 42,100 lower than a year earlier. However, on a seasonally adjusted basis, there was an increase of 11,200 during the month. This may reflect the ending of the PUP. In March, the official unemployment rate stood at 5.5 per cent of the labour force, compared to 7.7 per cent in March 2021.

While economic indicators are still strong, the Ukraine war and cost of living pressures now pose significant threats to Ireland’s wellbeing. We will discuss these issues in upcoming podcasts.

Tax Revenues (Quarter 1 2022)

Source: Department of Finance Fiscal Monitor, 6th April 2022.

Yes good to see you back, and am interested in what you said you would talk about. I am interested on how the West North West can be helped to keep up with the East

Good to see you back!! I was wondering when we’d see or head you again! All good with you both I hope?