How's the economy doing?

Irish economic snapshot

IRELAND – AN UPDATE ON THE DATA

Jim Power

This newsletter takes a look at some of the key economic data developments in the Irish economy so far in 2021. It is not exhaustive but provides a snapshot of some of the more interesting economic variables – or at least we think it does.

In overall terms the economy is generally doing ok in the circumstances, with obvious significant sectoral challenges. As the economy gradually opens up over the coming months there should be a strong rebound in activity, with international tourism the obvious casualty. Just continue to bear in mind that household savings increased by €15.7 billion in the year to February 2021, to reach a record high of €127.8 billion. That represents a lot of pent-up consumer spending power in the economy. The other point worth bearing in mind is the extreme resilience of the tax base, particularly the income tax base.

THE GENERAL ECONOMIC BACKDROP

Ireland has been subjected to stringent Level 5 restrictions since the end of December, which are only now starting to be eased in a very cautious and conservative manner. Throughout the whole ordeal over the past 14 months, one thing that has become more and more apparent is the very obvious dual nature of the economy and of the workforce.

If one works in or operates in sectors such as foreign direct investment (FDI) companies; the public sector, where no jobs have been lost and a pay increase of 2 per cent was delivered last October; financial services; and professional services, the last year has been pretty good from an economic and financial perspective. On the other hand, if one works in or operates in tourism, hospitality, non-essential retail, personal services, the airline industry, or arts & entertainment, it has been a dreadful environment.

In Ireland, and indeed around the world, it is very clear that manufacturing is doing very well, but many service sector activities are on the floor. No surprises there, as service sector activities have in the main been subject to the most stringent restrictions. Of particular note in Ireland is the fact that the Purchasing Managers Index (PMI) for manufacturing jumped to 60.8 in April, which is the highest reading since this series began in 1998. Suffice to say, manufacturing is booming in Ireland at the moment.

The Department of Finance published its Stability Programme Update (SPU), or in other words its latest forecasts for the Irish economy in April. GDP expanded by 3.4 per cent in 2020, making Ireland the only country in the EU to experience positive growth. However, this provides a distorted sense of the economy, because when distortions caused by multi-national activities are removed, modified growth (GNI*) contracted by 4.2 per cent. This provides a more realistic assessment of Ireland in 2020. An economy that was very good in some spots, and very bad in other spots.

The mandarins in the department are more optimistic about the second half of this year as restrictions are eased and as we return to a semblance of normality. Over the next 5 years, the expectation is that growth will steadily recover, and the labour market in particular will steadily improve. The budget deficit (General Government Balance) is projected to gradually improve, as is the level of government debt expressed as a per cent of the more meaningful measure of economic activity, GNI*.

All in all, the Department of Finance is relatively optimistic about recovery prospects, but the outlook is heavily contingent on positive epidemiological developments, and the risks are obvious. Table 1 summarises the key medium-term forecasts. Let’s hope it proves prescient.

Source: Department of Finance, Stability Programme Update, April 2021

THE EXCHEQUER FINANCES

In the first 4 months of the year, an Exchequer deficit of €7.63 billion was recorded, which compares to a deficit €7.47 billion in the same period last year. The €156 million deterioration in the deficit was caused by a significant increase in expenditure as a result of the COVID-19 response, rather than a deterioration in tax revenues. Gross spending by Government was up by 9.1 per cent or €2.2 billion, with spending on social protection up by €2.3 billion on the first 4 months of 2020.

On the tax collection side, tax revenues continue to hold up remarkably well, despite the COVID-related difficulties for the economy. Overall tax receipts were 4.2 per cent ahead of last year. The VAT increase reflects the total collapse in March and April 2020, while the increase of 6.2 per cent in income tax reflects the fact that high-paid workers who pay most of the income tax in our very progressive income tax system have been relatively unaffected by COVID-19. Lower paid workers, who pay little in income tax, are the ones who work in sectors that have been most adversely affected by the restriction in place. The strength of income tax take is quite remarkable, and is another indicator of the dual nature of the economy at the moment.

In the first 4 months of the year, income tax accounted for 49.5 per cent of the total tax take. This is up from just over 27 per cent in 2006. Let nobody claim that Ireland does not have an extremely progressive income tax system, or deny the fact that higher earners do noy pay a hell of a lot of income tax in this country.

The weakness in the corporation tax take is due to the fact that so far this year, €290 million has been withheld to make payments under the Covid Restrictions Support Scheme (CRSS). Were these receipts included, the corporation tax take would stand at €862 million, just €40 million lower than the same period last year. It is quite likely that corporation tax receipts will strengthen considerably this year and probably next, reflection the record earnings being reported by the US tech companies, who have a very significant presence in the Irish economy.

Source: Department of Finance, Fiscal Monitor, May 5th 2021.

COVID-19 has had and continues to have a dramatic impact on the public finances. At the end of 2020, the public debt to GDP ratio stood at 59.5 per cent, up from 57.4 per cent at the end of 2019. It is expected to reach 66.6 per cent at the end of 2021. The debt to modified gross national income (GNI*) ratio, which is the more realistic measure of economic activity, stood at 107.8 per cent at the end of 2020, up from 95.6 per cent at the end of 2019. This is projected to reach 114.7 per cent at end of 2021. In monetary terms, the public debt amounted to an estimated €218.2 billion at the end of 2020, up from €204.2 billion at the end of 2019. This is equivalent to €44,000 for every person resident in the State. This is amongst the highest in the developed world and is expected to increase to €47,700 by the end of 2021, with public debt projected to reach €239 billion. This debt legacy will have significant implications for Government expenditure and taxation policy for years to come.

THE HOUSING MARKET

This time last year as it was becoming more and more apparent that COVID-19 was about to wreak havoc on the Irish economy and the labour market, the consensus view was that Irish house prices would experience a welcome correction of perhaps between 5 per cent and 10 per cent. In the event, nothing could have been further from the truth.

Between February 2020 and February 2021, national average residential property prices increased by 3 per cent; average prices in Dublin increased by 1.2 per cent; and prices outside of Dublin increased by 4.7 per cent.

The explanation for this strong house price performance is that demand continues to exceed supply, with those who continued to do well in 2020 and managed to maintain earnings and grow savings continuing to fuel demand. On the supply side we had just 20,676 new dwelling completions. We need around 35,000.

Housing definitely represents the most politically important issue in Ireland at the moment and will have a major bearing on the outcome of the next general election. The latest housing initiatives from Government are not deemed sensible by many sensible people, and if this latest in a long line of strategies fails, there will be political hell to play. The lockdown of construction activity for the first 4 months of this year will not help the cause of Government, and the Minister for Housing who had all of the answers when in opposition. Now where have we heard that before?

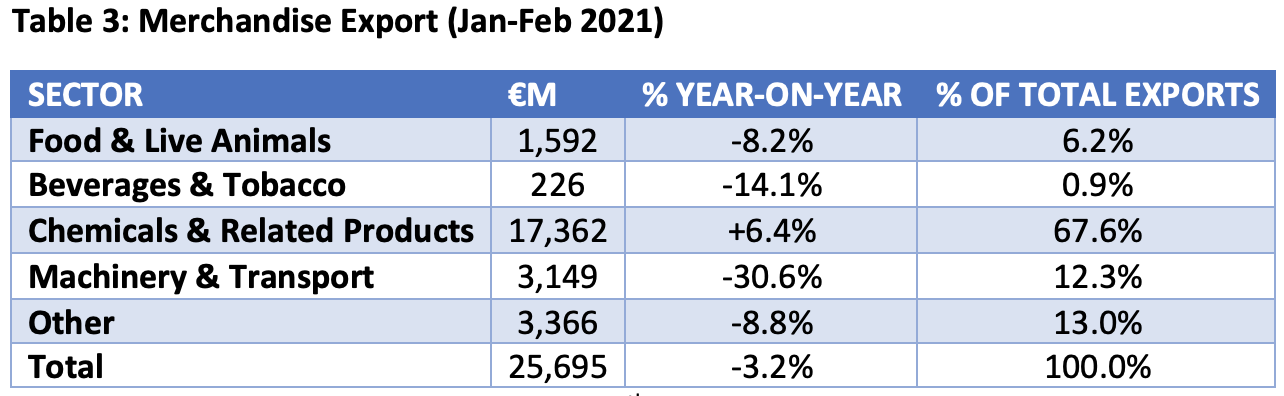

MERCHANDISE TRADE

Merchandise exports have been a key driver of Irish growth over the past year. However, pressures are emerging. In the first 2 months of the year, the total value of exports was 3.2 per cent lower than the same period in 2020. With the exception of chemical and pharmaceutical exports, which increased by 6.4 per cent and accounted for a very high 67.6 per cent of total exports, all other categories were weaker. There is clearly a Brexit effect at play here.

Source: CSO, Goods Exports & Imports, 15th April 2021

Exports to Great Britain declined by 12.1 per cent in the first 2 months of the year. Great Britain accounted for just 7.1 per cent of total exports, which is the lowest market share on record. Clearly, trade with the Great Britain has become much more difficult since 1st January, with increased delays, bureaucracy, and customs requirements. It remains to be seen if these are teething problems or a more fundamental structural alteration in the trading relationship with Great Britain. It is most probably a combination of both. It is also likely that importers in Great Britain stockpiled last year in advance of the Brexit deadline and we may now be seeing an adjustment for this stockpiling. It is also the case that one should not jump to too many conclusions based on just 2 months data, but the evolving situation will be watched with intense interest.

Source: CSO, Goods Exports & Imports, 15th April 2021

CONSUMER SPENDING

With non-essential retail shut down since the beginning of the year, it comes as no surprise that in the first quarter of the year, the overall value of retail sales was 4.9 per cent down on a year earlier. However, within this aggregate figure there are dramatic variations. The sale of food, beverages and tobacco was up 10.2 per cent on a year earlier, which is not surprising as we couldn’t visit restaurants. However, department store sales were down 40.9 per cent; clothing sales were down 58.4 per cent; and bar sales were down by over 88 per cent. These are dramatic numbers and are pretty much without precedent. At one level, the re-opening of non-essential retail later in May might just unleash a massive catch-up in behaviour, but the concern is that the foregoing data does not include online sales. Arguably the long-established trend in the migration to online, has been pushed forward by maybe five years over the past year, and many consumers might just not bother returning to the bricks and mortar shopping experience. This is a significant concern for the integrity of our village, town and city streetscapes. Hopefully, consumer will be minded to return to the physical shopping experience.

New car sales in the first 4 months of the year were 10.1 per cent up on the same period in 2020 at 55,207 new vehicles. However, the sector was effectively shut down in March of last year, but click and collect has been available this year, so the year-on-year comparison is flawed and needs to be interpreted carefully. New car sales in the first 4 months of 2021 were 24.4 per cent lower than the first 4 months of 2019.

Thanks Jim and Chris for the analysis, insights and caveats - as you say with the varying impacts across different sectors - the re-opening in 2021 and the unwinding of covid supports in 21/22 will be challenging and interesting to watch. Two questions I have - 1. the impact of a green deal for Ireland - is now the time to really kick-start it to benefit Irish society and all businesses and 2. your references to GDP and GNI (which are important distinctions and others should highlight them as well), I find Diane Coyle's work on GDP and it's flaws interesting and perhaps in a future podcast you could cover that topic. Regards Richie