Is the price of a pint a good inflation indicator?

Is the price of a pint a good inflation indicator?

Going out in London is harder on the wallet

Chris Johns

The price of a pint in my favourite central London pub has risen 10% since they were last open. One anecdote doesn’t constitute data but there are others. In that pub - and others - the price of the food has also risen by a double digit percentage since I was last there. In conversation with the staff it became clear that pubs and restaurants are finding it trickier than expected to hire staff and particularly difficult to find workers with experience.

My very subjective assessment is that while food prices have risen, food quality has fallen. Cramming a decade’s worth of experience into home cooking during a single year may have raised my own standards - restaurant quality may have just stayed the same while my expectations have risen - but I’m not so sure.

More generally, there are mutterings about economies reopening with shortages of skilled workers arising in several key sectors. Even in Europe. While unemployment may be high, skills shortages and mismatches could have an effect on the labour market that many surprise many economists .

Going out in London is now a much more expensive experience than it was before. Is this just a one-off thing and will it be restricted to the hospitality and entertainment industry? Much rests on the answers to those questions.

We knew that reopening would mean higher prices, particularly compared to a year or so ago when they were depressed by the pandemic. We liken the economy to a car: one that was taken off the road for a while and then suddenly restarted. As the tyres spin, some smoke is to be expected as pent-up spending power (with appetites to match) amount to hitting the accelerator a touch too hard. There are a lot of accumulated savings out there waiting to be spent.

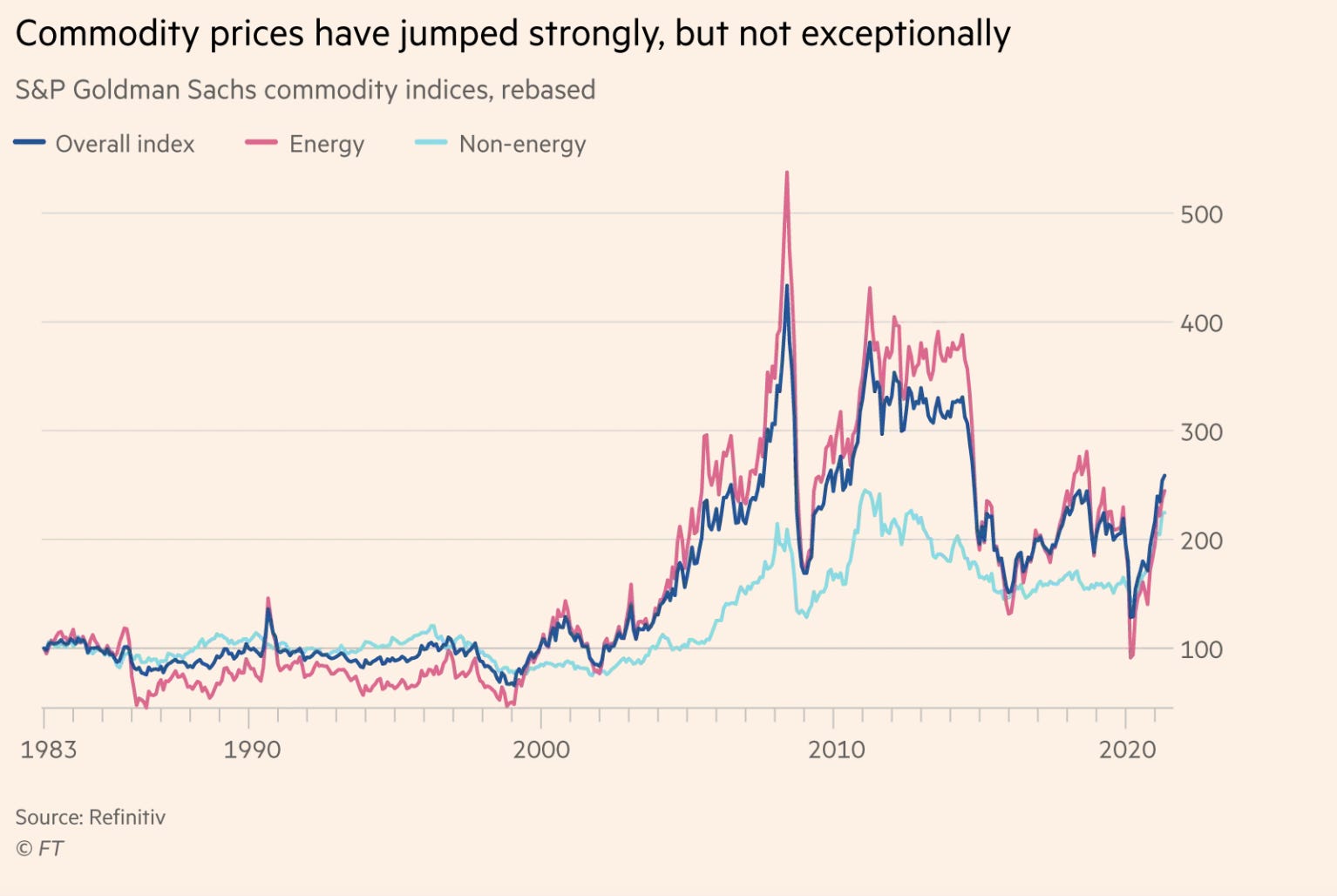

We are certainly seeing that ‘smoke’ in the form of raised prices on much more than a pint of beer. In particular, commodity prices are up across the board. As ever, the chief economics writer of the FT, Martin Wolf, has described all this in clear and persuasive terms. Here’s his chart of rise in commodity prices:

The title in Wolf’s chart makes the point: commodity inflation is here but needs to be put in context. There is an old cliche in financial markets that says that commodities are an asset class that you should occasionally rent but never own. Historically, they mostly go up for a while but, as the period from 1983-2000 shows, they can stay flat or go down for long periods of time. So the question naturally arises: is the spike seen this year - with some prices of key commodities doubling - likely to carry on, go sideways or even reverse. Should investors continue to rent these commodities or is it time to exit?

Overall inflation in the US spiked to 4.2% last month, the highest in 13 years and a bigger jump than expected. UK inflation also recently surprised on the upside. It’s not just the price of a pint.

Everyone has an opinion on all of this. Larry Summers, ex-US Treasury Secretary thinks inflation is going to be a problem - already is a problem. And that’s an opinion from someone who is normally in favour of economic stimulus. Nobel prize winner Paul Krugman thinks that inflation is a non-issue.

As Wolf says, there is an almighty amount of economic stimulus, probably unprecedented in scale, being thrown at a US economy that is already expanding very rapidly. Growing at a rate we normally associate with countries like China. Monetarists recoil with horror at the explosion in the money supply, caused by a central bank, the Fed, that has bought up around $5 trillion of mostly US government debt.

Wolf’s key insight is that what happens next depends more on politics than economics. Inflation is a choice: technically, while central banks can’t calibrate inflation to the nearest decimal point, they do have the tools to determine whether it is high or low.

Europe, largely under the influence of German political choices, typically runs with an inflation rate that is too low. That doesn’t seem likely to change very much. But what choice will the US make? Already, there has been a shift: more inflation has actively been encouraged with more to come. But how much more? That’s as much a choice for the Biden administration as it is for the Fed. It’s how fiscal policy will interact with monetary policy.

The simple fact is that nobody knows. These opinions should be held humbly and couched with all sorts of caveats. But that doesn’t get you headlines or speaking spots on CNBC.

Will that smoke (inflation) quickly dissipate as the car - the economy - restarts? Will the car’s speed settle down to a sustainable pace or will it accelerate into trouble - ever higher prices? If the price of a pint is anything to go by we all should be more worried than we were. My Irish friends may be looking enviously as we Londoners go back to the pub. When Irish pubs reopen my friends may be in for a surprise.