STRONG GROWTH IN 2021, BUT REQUIRES DEEP COMPREHENSION

THIS POST BY JIM POWER LOOKS AT LATEST NATIONAL ACCOUNTS DATA, EXCHEQUER FINANCES & UNEMPLOYMENT. A PICTURE OF BUOYANCY, NOTHWITHSTANDING THE THREAT POSED BY THE RUSSIAN ATROCITIES IN UKRAINE

STRONG ECONOMIC GROWTH IN 2021 AND A BRIGHT START TO 2022

By JIM POWER

ECONOMIC GROWTH IN 2021

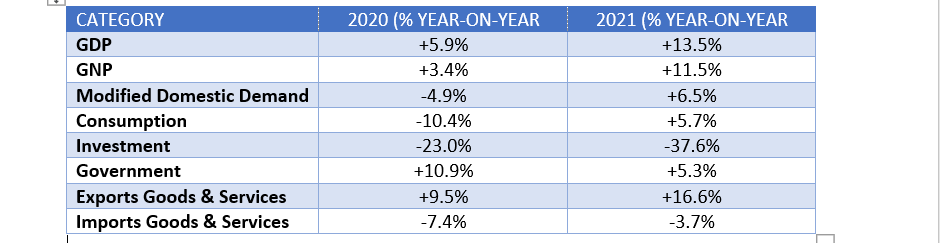

The CSO has just published the national accounts for the final quarter of 2021 and this gives us the first preliminary estimates of what happened in the full year. As is always the case with Irish national accounts data, there are serious distortions caused in particular by the activities of multi-national companies in areas such as intangible assets, which include intellectual property assets, and aircraft leasing activities. These items particularly distort the investment and imports of goods & services components of the national accounts. Comprehension is not easy. However, the clear message is that the economy rebounded strongly in 2021, but was dominated by the multi-national sector, but the domestic sector still delivered a decent performance. Output from multi-national corporations expanded by 21.9 per cent and output from the domestic components of the economy expanded by a respectable 5 per cent.

Gross domestic product expanded by 13.5 per cent, and when the net factor outflows, (mainly profit repatriation by multi-nationals operating here, as they send profits back to their shareholders) are taken into account, gross national product (GNP) expanded by 11.5 per cent. In 2021, net factor outflows totalled €110.6 billion, which is the highest level ever recorded. This reflects mainly the strong performance of multi-national corporations in 2021, which has been reflected in buoyant corporation tax receipts and a strong employment performance by IDA-supported companies.

National Accounts 2021

Source: CSO 4th March 2022

Modified domestic demand (MDD) seeks to measure domestic activity and includes consumer spending, investment activities when the multi-national induced distortions are adjusted for, and the contribution of Government, which was strong in 2021 due to increased Covid-related spending. This more realistic measure of economic activity expanded by a respectable 6.5 per cent, having contracted by 4.9 per cent in 2020.

In overall terms, the economy did well in 2021, but it is really important to acknowledge and factor in the dual nature of the economy and the distorted measure of activity that GDP represents in Ireland. Last year, GDP totalled €421 billion, which is a huge number for Ireland. Metrics like national debt and health spending are measured as a percentage of this grossly exaggerated number and look much lower than is really the case. Irish economic data cannot be taken at face value and require a deep dive to find out what is really happening in the real economy that most of us inhabit.

Along with the national accounts, the CSO included a table on employee compensation last year. Overall compensation of employees increased by 8.1 per cent, with ICT employees achieving growth of 13.7; those working in Professional, Admin & Support services saw growth of 12.4 per cent; construction saw growth of 11.9 per cent; and those working in Distribution, Transport, Hotels & Restaurants saw growth of 9.4 per cent. This is indicative of the buoyancy of the labour market and labour shortages.

THE EXCHEQUER FINANCES

What is happening on the tax collection side of the economy is always a good indicator of what is happening on the ground in the economy. 2021 was a very strong year in terms of tax revenues and this strong trend has carried over into the first two months of 2022. In the first two months of the year, an Exchequer surplus of €932 million was recorded, which compares to a deficit of €721 million in the first two months of 2021. The improvement of almost €1.7 billion really reflects the ongoing buoyance of tax revenues, but some cognisance has to be taken of the fact that the economy was subjected to significant Covid-related restrictions in the first two months of 2021. Notwithstanding this point, the underlying tax revenue situation is strong and is indicative of an economy that is doing well.

The key feature of tax revenues in the first two months of the year are:

· Overall tax revues totalled €10.1 billion which is 20.4 per cent or €1.7 billion higher than the equivalent period in 2021. The first two months of 2021 were distorted by restriction, and when compared to the first two months of 2020 (not impacted by Covid), tax revenues in 2022 were €900 million or 10 per cent higher.

· Income tax, corporation tax and VAT accounted for 82.9 per cent of tax revenues. Corporation tax receipts are always very low at this time of year, so no significance can be attached to corporation tax receipts at this stage of the year.

· Income tax came in at €4.7 billion, which is 16.8 per cent or €677 million ahead of 2021. The strength of income tax receipts reflects the very progressive nature of the Irish income tax system, and the high quality of employment being created in the economy. It is indicative of a very buoyant labour market, where retention, recruitment and increased labour costs are becoming significant challenges for many employers.

· VAT came in at €3.4 billion, which is 26.8 per cent or €712 million ahead of 2021, when a lower VAT rate applied on a temporary basis. When compared to the first two months of 2020, VAT receipts in 2022 are 10 per cent or €300 million higher.

Tax Revenues (Jan-Feb 2022)

Source: Department of Finance Fiscal Monitor, 3rd March 2022

The overall complexion of the public finances suggests that tax revenue buoyancy will be a feature of the economy in 2022.

On the labour market front, the lifting of restriction is impacting positively on the labour market. In February, the official unemployment rate stood at 5.2 per cent of the labour force, or 135,100 people. This is 45,000 lower than February 2021, when the unemployment rate stood at 7.5 per cent. When adjusted for Covid-19, the unemployment rate stood at 7 per cent of the labour force in February, down from 7.8 per cent in January and 27 per cent a year earlier.

The Ukraine war and cost of living pressures obviously now pose the key threat.