Summer in the CSO: Latest Irish economic data doesn't shine much light

Heaven for geeks

Jim Power

SUMMER ECONOMIC STATEMENT, THE HOUSING MARKET, NATIONAL ACCOUNTS AND EXTERNAL TRADE – OVERALL LOTS OF FUN STUFF FOR GEEKS

· The Summer Economic Statement cannot be described as remotely akin to austerity. The usual suspects are suggesting that this fiscal trajectory represents a return to fiscal austerity. Nothing could be further from the truth. Ireland has a dangerously high level of debt, and not attempting to rein in the budgetary parameters would be grossly dangerous and irresponsible

· Housing represents the most fundamental political challenge facing Government, and the outcome of the next General Election will be heavily influenced by the success or otherwise achieved by the incumbent government in addressing the housing problem. The problem was manifested this week by data on rents and house prices showing that both are still rising strongly.

· Ireland was one of the few countries in the world to record positive GDP growth in 2020, but caution is required in interpreting data. GDP grossly exaggerates the real health of the economy. GNI* is the better measure, but CSO has introduced us to another concept called NNI. CSO data are becoming the dream of geeks.

· Ireland’s exporters performing strongly, but Brexit effects still obvious.

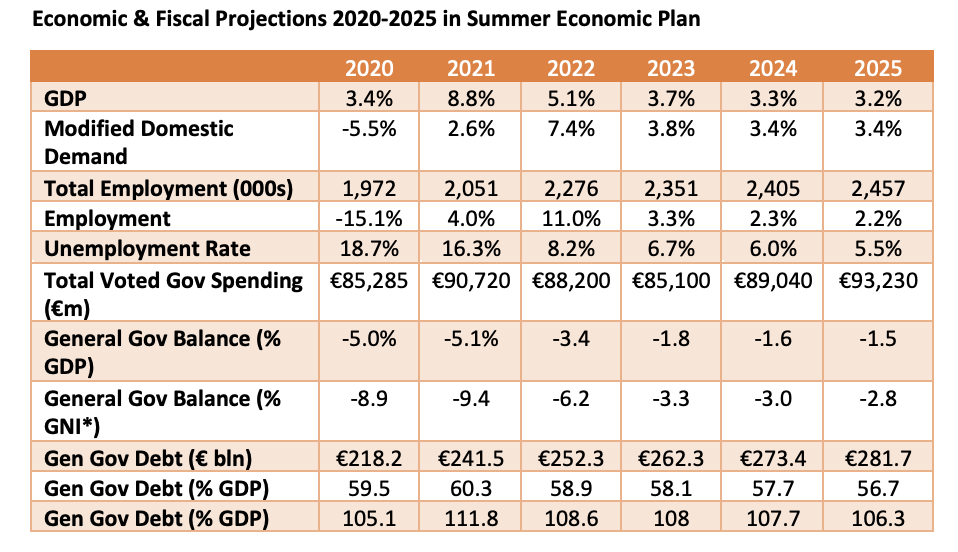

The Summer Economic Statement….

It has been reported in the media that the parties of Government were having some disagreement over the Summer Economic Statement and the amount of capital spending allocated to housing. In the event, the document was published on 14th July and sets out the Government’s medium-term budgetary strategy and explains the fiscal parameters against which Budget 2022 will be presented on 12th October.

Source: Department of Finance, 14th July 2021

The economic growth projections will be crucial to the achievement of the budgetary strategy. Growth is projected to rebound strongly in 2021 and 2022, before settling down to a trajectory that looks consistent with Ireland’s growth potential. These economic growth projections look realistic based on what we know at the moment.

A core budget package of €4.7 billion is targeted for Budget 22 which will be presented on 12th October. Of this total, €1.5 billion will be laid aside for new budgetary measures, with €500 million directed at tax changes and €1 billion for expenditure measures. Budget 22 will be a complicated affair and the real challenge for the Government will be to wean the economy off Covid supports, start the process of restring some semblance of order to the beleaguered public finances, and ensuring that economic recovery is supported. The Government is setting aside €2.8 billion for income, business and other supports should they be needed.

The debt objective is to stabilise the debt by 2023 and reduce it gradually thereafter. Have no doubt about it, Ireland’s government debt burden is now ominously high.

On the expenditure side, the Government is adopting an expenditure rule, whereby core (non-Covid) expenditure growth is tied to the estimated trend growth in the economy, adjusted for inflation. Government is going to allow permanent spending increase by 5% per annum in the post pandemic years. If achieved, this would be a sensible, albeit generous strategy.

Between 2022 and 2025, the Government intends to deliver €49.4 billion in capital spending.

The usual suspects are suggesting that this fiscal trajectory represents a return to fiscal austerity. Nothing could be further from the truth. Ireland has a dangerously high level of debt, and not attempting to rein in the budgetary parameters would be grossly dangerous and irresponsible.

Housing causing political disagreement within Government….

It should be clear to anybody with any semblance of a political antenna that housing will be the main factor that will determine the next general election. At the moment the basic political equation looks quite straightforward – solve the housing crisis, or at least being seen to be making progress would pay political dividends, and failure to make progress could exact a significant political price.

Data published this week does highlight the nature of the challenge.

Rents continue to rise and rental affordability is strained….

The latest data from the Residential Tenancies Board (RTB) show:

• National rents grew by 4.5% year-on-year in Q1 2021 in comparison to 4.7% in Q1 2020

• Outside Dublin, year-on-year rent inflation stood at 7%, while in Dublin inflation was 2%.

• The national standardised average rent stood at €1,320 in Q1 2021, an increase of €33 compared to the previous quarter.

• In Q1 2021 in Dublin, the standardised average rent stood at €1,820 per month, a 2% increase year-on-year, while the lowest monthly rent was in Leitrim at €596 per month, a 3.8% year on year increase.

• Affordability remains a significant issue with tenants paying on average 36% of their disposable income on rent.

• In Dublin, 64% of tenants indicated that they spend more than 30% of their net income on rent.

House prices continue to rise…

The latest house price data from the CSO suggests that house prices continue to go ahead in a vigorous fashion. The key takeaways from the May Residential Property Price Index are:

• National average residential property prices declined by 55.2% between the peak of the market in April 2007 and the low point of the market in March 2013. Between March 2013 and May 2021, prices increased by 92.9%. National average prices in May 2021 were 5.5% higher than a year earlier. The national house price index in May 2021 was still 13.5% lower than its highest level in May 2007.

• In the Rest of Ireland (excluding Dublin), average residential property prices declined by 56.5% between the peak of the market in May 2007 and the low point of the market in May 2013. Between May 2013 and May 2021, prices increased by 93.2%. Prices in May 2021 were 6.2% higher than a year earlier. Despite the recovery, prices outside of Dublin in May 2021 were still 16% lower than their May 2007 peak.

• In Dublin, average residential prices declined by 59.6% between the peak of the market in February 2007 and the low point of the market in February 2012. Between February 2012 and May 2021 prices increased by 101.2%. Prices in May 2021 were 4.9% higher than a year earlier, but average prices in Dublin were still 18.8% lower than their February 2007 peak.

The housing market is indeed hot, and the political pressure is growing. The Fianna Fáil housing minister presents the Housing for All Strategy next week….let’s hope it makes sense.

CSO national accounts data show that Ireland was indeed one of the few countries in the world to experience positive GDP growth in 2020, but this headline comes with a serious health warning….

The CSO has just published revised growth numbers for 2020. Although historical at this stage, it does demonstrate the very unusual structure of the Irish economy, and the very pronounced dual performance in 2020, which continues in 2021.

• GDP expanded by 5.9%.

• GNP expanded by 3.4%.

• Gross National Income * (GNI*), which is a more accurate measure of economic activity that strips out the impact of globalisation effects that seriously distort Irish growth numbers, contracted by 3.5%.

• In absolute terms, GDP in 2020 totalled €372.9 billion, but GNI* is €164.7 billion lower at €208.2 billion.

• Unfortunately, GDP is the international metric used for basis of comparison and against which important metrics such as budget deficits and Government debt are measured. The reality is that GDP seriously distorts the true health of the Irish economy, and GNI* gives us a much truer reflection of real life on the ground in the economy. It is also the case that Ireland’s fiscal situation is much worse than the official data expressed as a % of GDP suggest. This may look like stuff for geeks, but the real impact on lives and future policy is very important to understand.

• The CSO has announced another measure of economic activity called Net National Income (NNI) at constant prices. This measure is defined as Gross National Income (GNI) less the amount charged for the consumption of capital assets, including Intellectual Property assets. It is an important measure of underlying economic activity that strips out the distortionary impacts of globalisation, which are pretty extreme in the case of Ireland, and it closely resembles GNI*. NNI contracted by 4.3% in 2020.

Revised first quarter growth data show that the distorted nature of Irish growth statistics is still alive and well…

GDP increased by 10.7% on a year-on-year basis, but domestic components such as consumption very weak due to Covid restrictions. The annual decline of 4.8% in modified domestic demand instructive, but the export performance of the multi-national sector continues to be very buoyant.

Brexit continues to impact on Irish trade…

In the first 5 months of 2021, the total value of exports was 3.1% lower than the same period in 2020. Supply chain issues, COVID-19. Global growth and Brexit are all impacting. However, despite the overall decline, the export performance continues to be very strong in challenging circumstances.

Exports to Great Britain increased by 11.6% in the first 5 months of the year. Great Britain accounted for 8% of total exports. Exports to Northern Ireland increased by 38%. The Northern Ireland protocol is good for all-island trade.

There is clearly a Brexit effect on trade between Ireland and Great Britain in certain sectors. Of the exports to Great Britain in the first 5 months, Chemicals & Related Products increased by 29.4%, but exports of Food & Live Animals were down by 9.1%. However, in the month of May, exports of food and live animals to Great Britain were up by 24.4%. This suggests that some of the teething problems are being ironed out.

On the import side, overall imports from Great Britain in the first 5 months were down by 35.3%, with food and live animal exports down by 50.6% or €613 million.

Thanks Jim for the detailed analysis. It's good that you and Chris discuss the differences between GDP and GNI* with an emphasis on GNI* - I don't hear that from other commentators and bearing in mind what you're saying about Government debt - GNI* is the 'proper' measure. A suggestion - with the GNI* vs GDP in mind - it would be great if you could have Sebastian Barnes (IFAC) on the podcast discussing his and your views on this topic. I heard him recently on Irish Times Inside Business podcast and he provides an interesting perspective. Cheers