The empire strikes back - at least, Bitcoin enthusiasts try to

Deconstructing Niall Ferguson

Chris Johns

We always get lots of pushback when we speak about Bitcoin and all things crypto. Mostly, we get enthusiasts telling us why we are wrong to be sceptical. One or two people actually agree with us, but our postbag doesn’t contain many missives of that kind. With us or against us, the exchanges are, for the most part, polite and detailed.

Occasionally, the responses verge on deranged - but often have common themes. The clue usually comes with a big reveal: somewhere in the invective, usually hiding in plain sight, is hatred of government and love of libertarianism. Or something that passes for for these (classical libertarians wouldn’t be seen dead in the company of Bitcoin fans, they are much more choosy about their anarchist friends).

Bitcoin is one of those slippery concepts that annoyingly allow the analyst to get close to understanding, but never all the way. Take the concept of ‘value’ - as financial types often ask, ‘what is Bitcoin’s value proposition?’. A marketer puts the same question slightly differently, ‘what’s the unique selling point?’

Different people answer this question in many and varied ways. Those libertarians think that anything not involving government has to have value. Other focus on scarcity: Bitcoin will never exceed a certain number of coins issued. A hatred of banks and all traditional forms of financial intermediation also, it is argued, adds to crypto’s value, albeit in somewhat vague and nebulous ways.

If something has value, we (financial analyst types) traditionally assume that value can be measured. For financial assets, value is usually measured via price. Oscar Wilde, of course, taught us that a cynic is one who knows the price of everything and the value of nothing. Once you assert that value cannot be measured, at least objectively, then it becomes anything you want it to be.

The definition and measurement of value has occupied the minds of philosophers and economists for thousands of years. In a recent (long but readable and highly recommended) book, ex-Governor of the Bank of England, Mark Carney, takes us on a tour of how value has been defined and re-defined and argues that we are very confused between value and values (another way of making Wilde’s original point). At the very least, Carney points out, multiple times, how our perception of value changes all the time. The huge Canaletto on one wall of the Bank Governor’s office turns out not to have been painted by the (or any) Italian master..

That point about the difference between value and values must, I would assert, appeal to crypto enthusiasts. If it’s all about value - price - then things are not going too well. Something as volatile as Bitcoin is not a good store of value (something that we usually think any form of money should have). At least part of crypto’s appeal must be subjective - all that libertarian hatred of government and banks, or something like that. Subjective beauty always being in the eye of the beholder. That sort of thing.

Some crypto devotees are worried about the recent price gyrations (mostly falls). In a recent long and rambling defence of all things Bitcoin, eminent historian Niall Ferguson takes us through his vision of sunny uplands for crypto. (H/T The Other Hand reader, James O’Sullivan.)

To his credit, Ferguson takes on the basic problem head on:

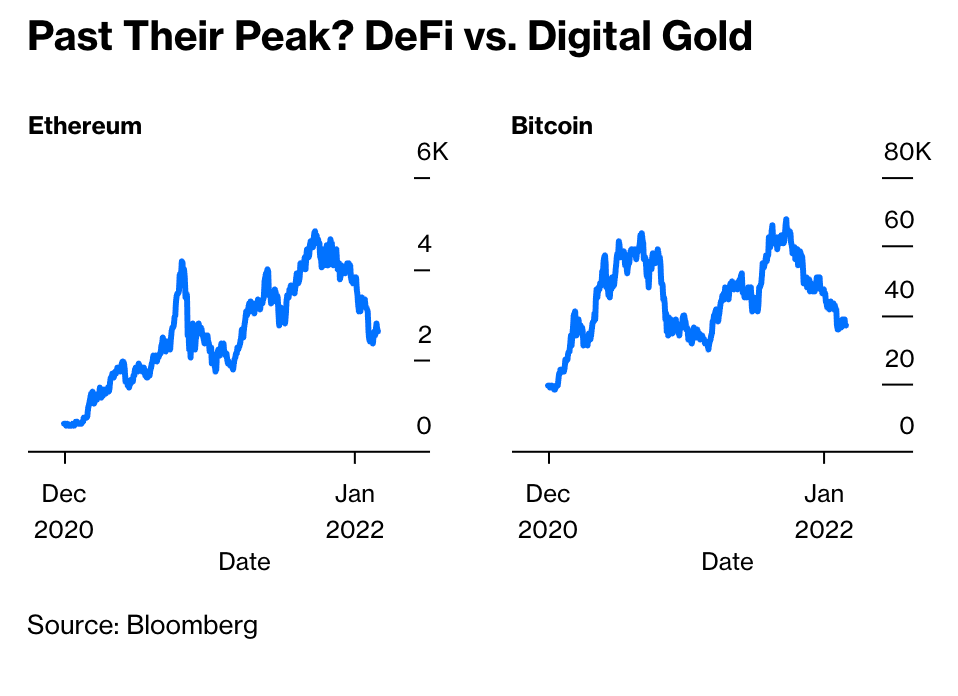

That’s a lot of recent price (if not value) fall. By the way, that ‘DeFi’ in the title of the chart is a reference to ‘Decentralised Finance”, something I’ll come back to.

Acknowledging that crypto prices have fallen is quickly followed by Ferguson with a half-hearted (and unconvincing) swipe at one the biggest and most high profile critics of Bitcoin, Nouriel Roubini, known if nothing else for coining (sorry) the word ‘shitcoin’. Ferguson’s bete noire is, in fact, Nobel prizewinning economist Paul Krugman - the two have regularly clashed and this piece is no different. In a pattern familiar to regular readers of Ferguson, this swipe at his critics is quickly followed (and peppered throughout his article) by ‘look at all the times I correctly forecast X’. I can only think it’s academic insecurity.

Ferguson goes back to Bitcoin, after this rather lengthy digression away from the fundamental problem (the recent large falls in price) with two reasons why he thinks more large falls in price are unlikely. First, Bitcoin has become very big: its value, at least measured by its price times the number of coins in circulation, surpassed $1 trillion last summer (before falling back somewhat).

The idea that because something is big means that its price can’t fall by a lot is, I would argue, a spectacularly thin piece of reasoning. Facebook (or, to be more precise, Meta) was also worth not too far from $1 trillion just before a near 25% fall in recent days. There are plenty of other examples of large companies, highly valued assets, flying too close to the sun. Size is no guarantee of performance.

Next, Ferguson suggests that Bitcoin is, in fact, less volatile than it used to be. He backs this up with a chart of volatility averaged over 30 day periods.

Investors don’t like volatility, particularly those with a short time horizon. And there are, for the most part, only two types of investor: short term ones and fibbers.

While Ferguson is 100% correct about the fact that Bitcoin’s volatility has fallen compared with the level seen in 2014, there is no guarantee that it will stay fallen. Past performance is no guide to the future and all that. In addition, just look at the average level of volatility over the last decade: crudely (by eye), it looks to be about 70% (at least). My rough calculation of the (monthly) volatility of the US stock market comes in at around 17%. I’ll just leave that there.

Ferguson goes on to discuss the fallen stars of 2021 ( the likes of Gamestop and Peloton) and the diverging performances of Apple, Google, Amazon and Microsoft versus facebook (Meta). He’s absolutely right when he points out that kids have been deserting Facebook for ages: it has, in my estimation, become a platform for oldies. What any of this has got to do with crypto escapes me. I think a trick is missed by failing to mention that Libra, facebook’s excursion into crypto, was abandoned a tad too quickly.

We manage to get back to Bitcoin with an attack on the Federal Reserve and rise of global inflation. Regular listeners to The Other Hand will be familiar with this story. Here we get Ferguson’s assertion of Bitcoins key value proposition:

As my [Ferguson’s] Hoover Institution colleague Manny Rincon-Cruz argued in a brilliant essay last month, “Bitcoin’s core value proposition, and technological innovation, is digital scarcity via a public, decentralized ledger that tracks a fixed supply of 21 million bitcoins.” It’s that scarcity that investors like, compared with — as the pandemic made clear — the potentially unlimited supply of fiat currencies.

The story here is absolutely clear: Bitcoin has value because it is scarce. And technology something ledger something (that’s the subjective bit, I think).

Bitcoin is worth something because governments can’t produce it and its supply is fixed, unlike dollars, pounds or euros which can be printed in infinite amounts.

I could argue that I’m not a product of the government and that I am also in short and fixed supply but have little value, at least according to the fees I charge for this article. But that would be churlish. More to the point, scarcity is never enough for something to have value at all times - sometimes it is, sometimes it isn’t.

Ferguson likes the idea that Bitcoin is playing the role of gold in the 1970s. Gold, for some people, is an inflation hedge. This has sometimes been true but not always. Gold has existed forever but the 1970s happened only once - and, at risk of making a forecast, Ferguson is wrong if he thinks the experiences of that decade are about to be repeated. To be fair, he talks about the 1970s as if he is worried about a repeat and then appears to contradict himself with an assertion that they won’t happen again. I really do wish I could charge for writing this kind of stuff.

Anyway, whether or not the 1970s are back, for the record, I thought it was a fabulous period. The music alone justifies its claim to be the greatest decade ever. And if gold is the inflation hedge against 1970s-style inflation why do we need another asset that protects us from inflation?

Ferguson then digresses into an odd discussion of centuries of bond market history.

The discussion is strange because he seems to think that the data in the chart can tell us something about what will happen next. The trouble with charts is that they almost always say nothing about the future: that’s the nature of data. The data in the chart is intrinsically fascinating, merits close study and the original author deserves plaudits.

But the chart says that bond yields can, over the short term (often lasting years) do anything. Unless you combine a model with your data you can’t say anything meaningful about the future. I guess historians have got to talk about history and somehow link the past to the future in predictive ways. All very unconvincing if you ask me.

I’ve read and re-read Ferguson’s article to see the connection between crypto’s bright future and seven centuries of real interest rates but I’m afraid I failed. My bad.

We finish with an excursion into NFTs, DeFi and a bit of a kitchen sink approach to modern financial jargon - mention of much of it as you can. Might impress the reader. It’s all a bit of a mess, at least in my eyes. I think the point is that technology is disrupting traditional finance with much more to come.

This is absolutely right but I don’t see any automatic link to crypto. Cash is disappearing and once Central Banks issue their own digital currencies we will see traditional retail banks disappear (which is why the central bankers are being so slow to issue them - what will they do when they don’t have high-street banks to regulate?).

I don’t wish to appear to be mean to Ferguson. But his rambling piece is not a sturdy defence of crypto or a convincing statement of Bitcoin’s value proposition. I could do that - but that would be an excursion into subjective value theory. Subjective value is important and could mean that Bitcoin and some/all the rest of the coins stick around for a long time. I have no idea. But all that volatility seems likely to stick around for as long as these things exist.

Very good, Chris (and Jim). William Manchester tells us where feudalism can take us: https://en.wikipedia.org/wiki/A_World_Lit_Only_by_Fire.

You are brave to address this important topic. Thank you!

Great article Chris and kudos for addressing some of the issues with crypto. Who knows how it will play out. Your paragraph on CBDCs may overlook the fight the high street banks will put up against CBDCs. They will not want to be disintermediated. There's a great interview with Yanis Varoufakis, a fellow crypto sceptic, about all these issues: https://the-crypto-syllabus.com/yanis-varoufakis-on-techno-feudalism/amp/